feature

Industrial distribution: 2024 year in review

Key trends, M&A activity and investment trends.

By Brad Williams

2021 Leader Graphic Studio / Creatas Video / Getty Images

The industrial distribution sector had an active year in 2024, caused by changes in macroeconomic regulations, supply chain adjustments, extreme weather, and shifts in M&A activity. Due to matters such as geopolitical instability, interest rate uncertainties, labor shortages, and increased demand for domestic manufactured goods, industrial distributors had to adapt to changing market conditions.

This report summarizes the trends that impacted industrial distribution, including:

- Looming tariffs and their influence on costs and supply chains

- Macroeconomic influences on industrial distribution

- The effect of extreme weather on supply chains and inventory management

- Labor shortages and workforce challenges

- Consolidation and competitive forces in the industry

- M&A activity Investment Trends

Key trends and market influences

Macroeconomic environment

- Interest Rates & Inflation: The Federal Reserve maintained higher interest rates for the majority of the year, influencing borrowing expenses and structures of M&A transactions.

- Onshoring & Domestic Production: Incentives provided by the government on domestic production raised demand for industrial materials, favoring electrical and plumbing distributors on infrastructure projects.

- Consumer Spending & Construction Slumps: Rising borrowing rates influenced commercial construction, increasing demand for electrical and plumbing materials.

- Regulatory Pressures: Complying with environmental laws and energy efficiency codes influenced procurement practices, particularly in HVAC and lighting distribution.

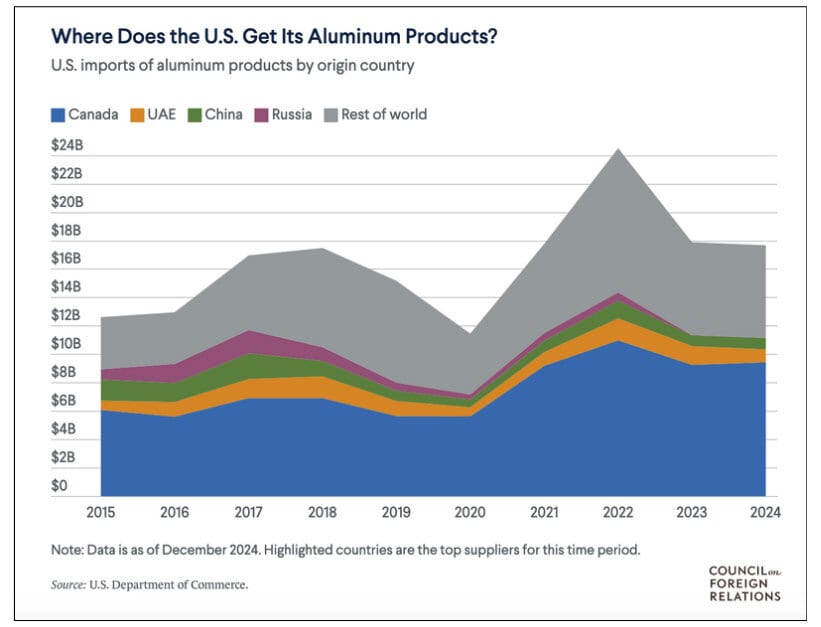

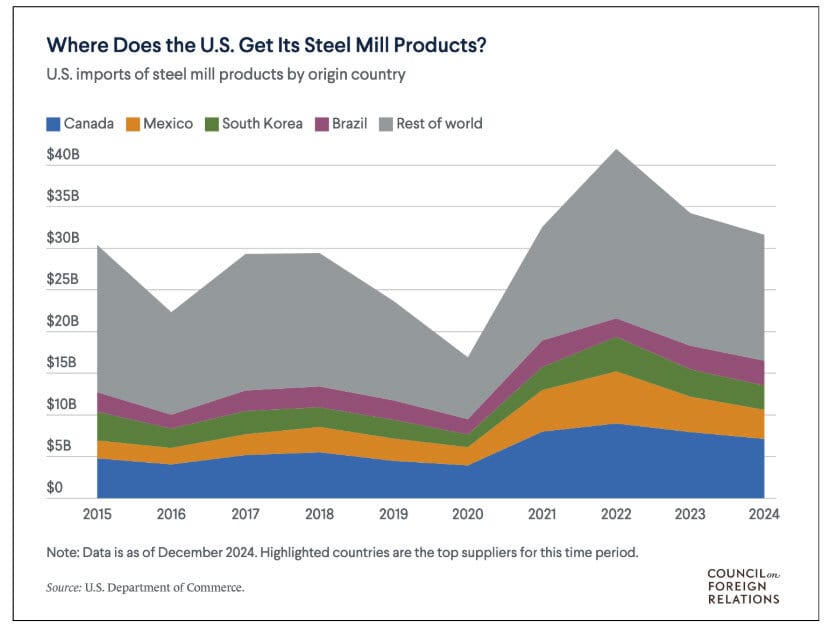

Pending tariffs and supply chain impacts

- The threat of new tariffs on imported materials kept industrial distributors in limbo, particularly those companies that rely on steel, copper, aluminum, and electrical components.

- Plumbing and HVAC producers that imported raw materials from abroad were potentially facing increased expenses, leading to pre-buy stockpiling behavior.

- Distributors adjusted sourcing practices, turning to domestic suppliers to mitigate tariff-induced cost hikes.

- Some companies levied higher prices to consumers, while others absorbed the costs in a bid to maintain pace with rivals, impacting margins in industrial sectors.

- Tariffs making inputs more expensive would result in distributors accumulating larger inventories in order to gamble against higher future prices. Inventory jumps are probable, but companies must balance short-term purchasing tactics against long-term fiscal prudence in order to avoid liquidity issues.

- Tariffs could impact distributors' and manufacturers' cost of goods sold (COGS), but they will not impact M&A. The forces driving deal flow, strategic expansion, vertical integration, and private equity investment are still intact.

- Many owners of industrial companies are already planning to exit on account of age, industry consolidation, or capital market trends. Tariff uncertainty would render such plans even more imperative, compelling owners to exit before the costs push up to detrimentally affect valuations. However, tariffs will not force owners to sell, but they could be the trigger for those considering an exit, resulting in more succession-driven M&A transactions.

- While tariffs affect inventory strategy and COGS, they will not slow M&A activity significantly. M&A remains driven by underlying business needs. Except in the event of a structural capital market realignment, deal flow will not fall significantly due to tariffs. Industrial business owners should expect the value of their businesses to grow when tariffs increase the cost of goods sold (COGS).

Labor shortages and human resource problems

- There remained an endemic shortage of skilled labor impacting industrial sectors, particularly plumbing, electrical, and restoration sectors.

- Contractors and distributors struggled to find competent assistance, leading to longer schedules and increased labor costs.

- HVAC and plumbing companies allocated resources in the form of training programs, apprenticeships, and automation equipment to make up for the shortfall.

- Logistics and transportation companies dealt with wage inflation and recruitment pressures, driving more use of AI-driven logistics control and warehousing automation.

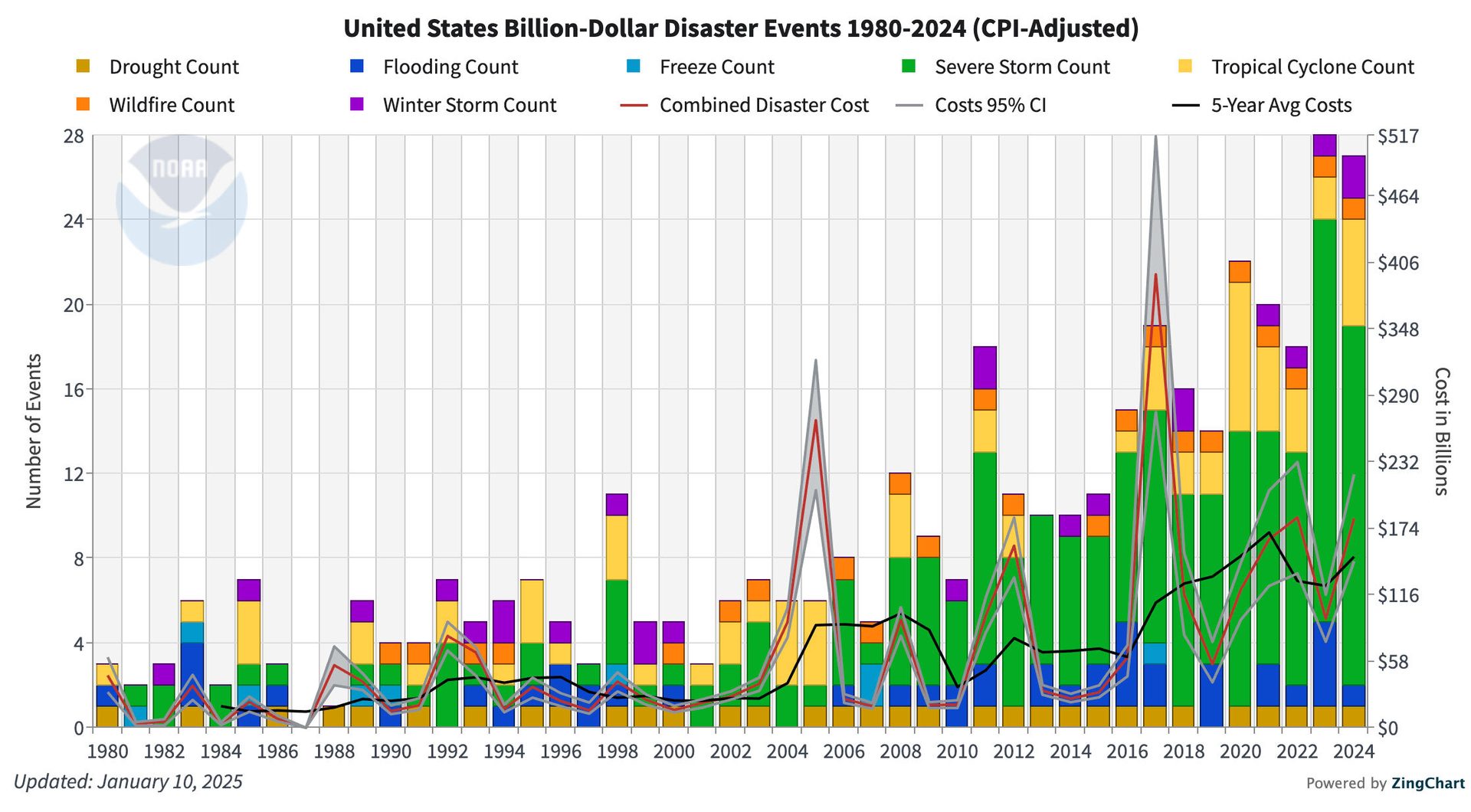

Extreme weather and industrial distribution

- Last year, there was an increase in weather disasters like hurricanes, floods, and wildfires, which affect industrial companies’ logistics and supply chains

- Electrical distributors saw an increase in demand for standby power solutions due to storm-caused power failures, while plumbing and HVAC suppliers saw greater restoration and infrastructure project sales from severe weather events.

- Restoration companies experienced an increase in demand for the services of dehumidifiers, insulation, and plumbing emergency services as increased property damage claims were filed.

- Logistics and transport operators were forced to adapt to extreme weather, rising costs, and compromised delivery reliability.

Consolidation industry

- The tide of big entities acquiring smaller niche distributors became even stronger in 2024 and created fewer sole sellers of electrical, plumbing, and restoration distribution.

- National players grew geographically, so mid-sized regional businesses had to grow or go niche market to compete.

- Private equity firms continued to acquire industrial distribution platforms, seeking companies with strong recurring revenue models and highly complex supply chains.

- Consolidating businesses utilized digital transformation and supply chain efficiencies to create competitive advantages in an increasingly consolidated marketplace.

NOAA’s National Centers for Environmental Information (NCEI)

M&A and investment trends

- Strong Deal Flow: Despite economic uncertainty, industrial distribution M&A activity was stable with strategic consolidations and private equity investment propelling it.

- Private Equity Trends: PE participants concentrated on niche industrial distributors with compelling market positions and recurring revenue streams, particularly in plumbing, HVAC, and electrical segments.

- Key Transactions: Certain high-profile transactions redefined the competitive landscape, as market leaders extended through bolt-on acquisitions and strategic partnerships.

- Valuation Adjustments: Certain deal structures shifted because increasing interest rates raised the cost of capital, and earn-outs and seller financing were increasingly employed in transactions.

- Cross-Sector Consolidation: Cross-border transactions among contiguous industries expanded as companies sought to leverage adjacent capabilities, e.g., combining HVAC and electrical distribution capabilities to expand product offerings.

What This Means for Industrial Distributors

- Resilience and Adaptation: Industrial distributors must be resilient and adjust to macroeconomic environments, regulatory climates, and supply chain pressures.

- M&A Opportunities: Consolidation continues in the industry, offering opportunities for strategic acquisition as well as private equity investment.

- Technology as a Differentiator: Companies investing in digitalization, AI-driven stock management, and e-platforms will build a differentiation advantage.

- Resolution of Labor Issues: Labor shortages call for creative solutions, including investment in training, automation, and competitive pay offers to employees.

Tariff uncertainty could render exit plans even more imperative, compelling owners to exit before the costs push up to detrimentally affect valuations. However, tariffs will not force owners to sell, but they could be the trigger for those considering an exit, resulting in more succession-driven M&A transactions.

Planning ahead for 2025

- Stabilizing Interest Rates: Federal interest rate changes predicted by the Fed can affect the availability of capital for M&A transactions.

- Investment in Infrastructure: Federal and state government spending on infrastructure investment will drive industrial distribution demand.

- Technology Integration: Companies will become more sophisticated in their applications of AI and automation to enhance supply chain effectiveness and customer engagement.

- Geopolitical Forces: Foreign trade relations and global economic conditions could provide distributors with levels of complexity or opportunity.

Conclusion

Despite economic and regulatory challenges, the industrial distribution market was strong in 2024, led by M&A activity, private equity investment, and strategic growth initiatives driving the market. The outlook for 2025 is also positive, driven by infrastructure spending, technological advancements, and continued consolidation. At The Beringer Group, we continue to advise clients through this evolving environment, positioning them to capitalize on future opportunities and deliver maximum value to the market.

ABOUT THE AUTHOR: